")

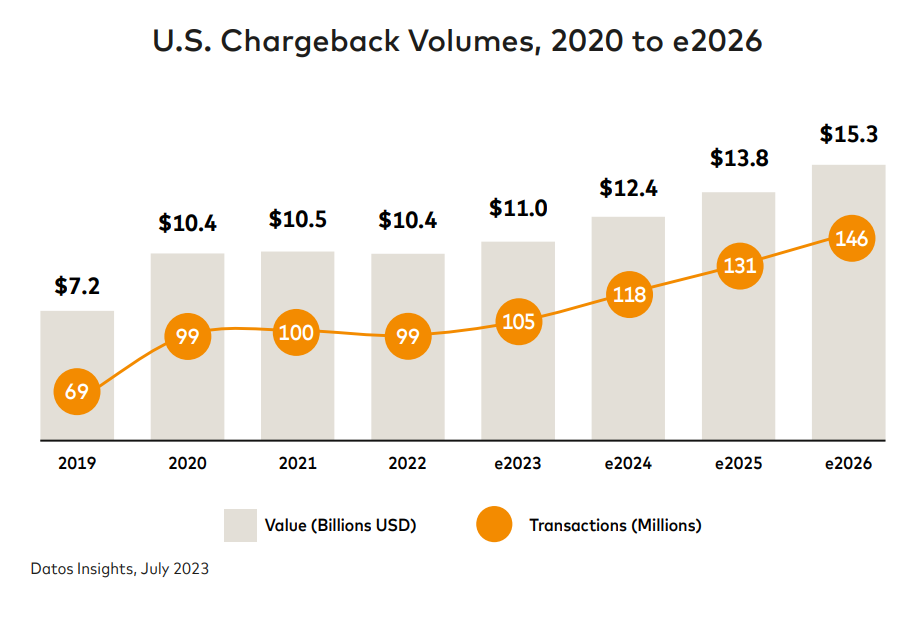

In the world of e-commerce and digital transactions, chargebacks are a significant headache for merchants. Cardholders dispute a transaction with their bank, resulting in a reversal of funds. Last year, the payment business suffered an estimated 238 million chargebacks. This volume is expected to increase by 42% to 337 million chargebacks by 2026. With an estimated chargeback volume of 105 million in 2023, the US holds the lion’s share of global chargebacks. Chargebacks cost US merchants $243 billion in 2023.

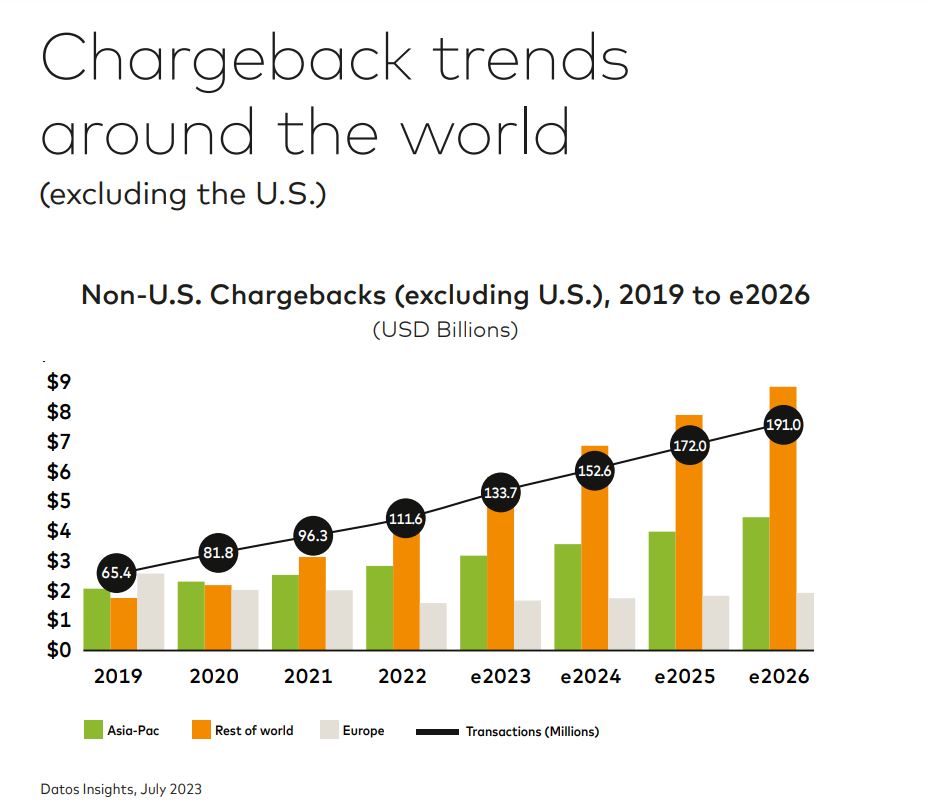

As can be seen in the graph below, Europe’s future chargeback volumes are expected to be relatively stable. This is most likely due to the EU requiring that businesses adopt SCA tools like 3DS to authenticate transactions for digital payments.

Recent statistics cited by Mastercard revealed a 32% year-over-year increase in chargebacks, supported by Visa reports underscoring this rising threat, showing that up to three-quarters of all chargebacks filed were cases of friendly fraud or first-party misuse.

While there are different chargeback scenarios, merchants must understand the most common ones and implement effective prevention strategies to protect their businesses. Here, we will explore the top chargeback scenarios and strategies merchants can employ to reduce chargebacks.

Chargeback Scenarios

Fraudulent Transactions:

One of the most prevalent chargeback scenarios is fraudulent transactions, where stolen card information is used to make unauthorized purchases. In this case, both the cardholder and the merchant are victims of Fraud. Merchants should implement robust fraud detection tools, such as address verification systems (AVS) and card verification value (CVV) checks.

- Machine learning algorithms and AI-powered fraud detection platforms help merchants identify suspicious activity in real time and prevent fraudulent transactions before they occur.

Friendly Fraud:

There is nothing friendly about Friendly Fraud or First-Party Misuse. This occurs when customers intentionally dispute legitimate transactions just to get a refund of their payment for products or services they did receive. To prevent this, merchants should keep detailed transaction records and documentation to support their case in case of a dispute.

- Offering excellent customer service and support, including prompt responses to inquiries and complaints, can help resolve issues directly with customers and prevent them from resorting to chargebacks.

Unrecognized Transactions:

Cardholders may dispute charges if they do not recognize or remember making a particular purchase. To mitigate this risk, merchants should ensure that their billing descriptors are clear and recognizable on cardholder statements.

- Providing detailed order confirmations and receipts, along with clear product descriptions and shipping information, can help reduce confusion and minimize the risk of unrecognized transaction disputes.

Product or Service Not as Described:

Chargebacks occur when customers receive products or services that do not meet their expectations or are not as described in the pictures in the web shop. To address this, merchants should strive to provide correct and detailed product descriptions, including images, size, and detailed specifications.

- Implementing a transparent and customer-friendly return and refund policy can also help mitigate disputes related to product quality or dissatisfaction.

Billing Issues:

Discrepancies in billing, such as duplicate charges or incorrect billing amounts, can lead to chargebacks. Merchants should regularly review their billing processes and systems to ensure accuracy and consistency.

- Providing clear and accessible billing information, including invoices and receipts, can help customers understand and verify their charges, reducing the likelihood of billing-related disputes.

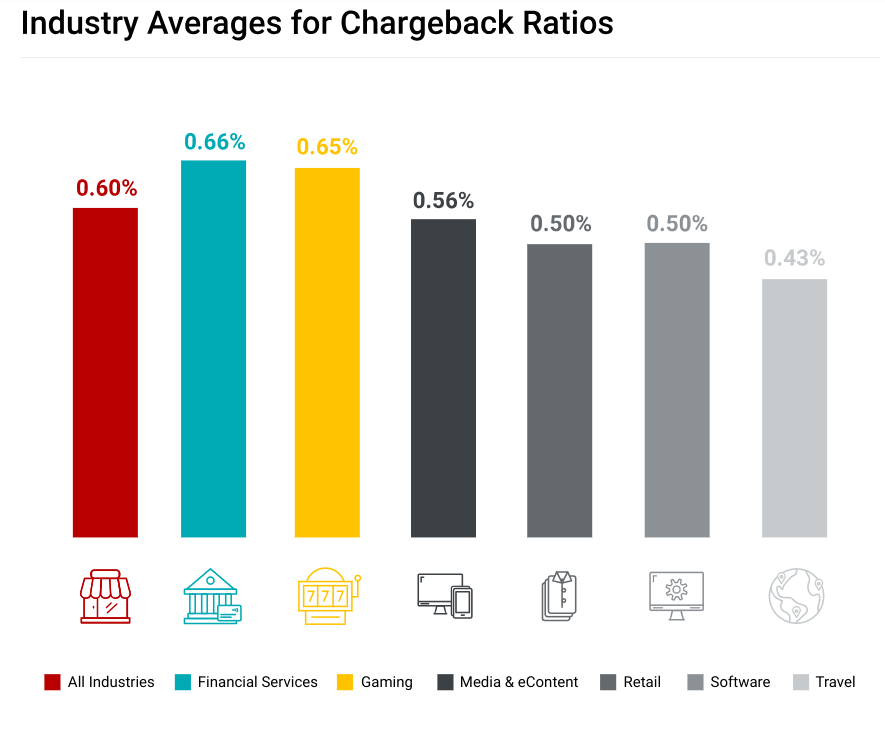

Merchants must implement strategies to improve their chargeback rate. For example, if you get 1000 chargebacks a month on 10.000 transactions a month, your company suffers a 1% chargeback rate. This lowers your conversion rate, not to mention other costs. Each card brand applies different chargeback thresholds. Chargeback ratios also differ per industry.

Source: Chargebacks911

Strategies for Merchant Protection:

- Implement Fraud Prevention Measures: Use fraud detection tools and technologies to identify and prevent fraudulent transactions before they occur.

- Optimize Customer Communication: Provide clear and accurate product descriptions, billing information, and order confirmations to minimize confusion and disputes.

- Offer Transparent Policies: Set up transparent and customer-friendly return, refund, and cancellation policies to address customer concerns and prevent chargebacks.

- Maintain Comprehensive Documentation: Keep thorough records of transactions, including order details, shipping information, and customer communications, to support your case in case of a dispute.

- Provide Exceptional Customer Service: Offer prompt and responsive customer support to address inquiries, complaints, and disputes effectively, reducing the likelihood of chargebacks.

Payment Service Providers (PSPs) play a crucial role in helping merchants prevent chargebacks by offering a range of value-added services (VAS) and solutions tailored to address various aspects of chargeback management and prevention. Here are some key added-value services that PSPs commonly offer to merchants to prevent chargebacks:

Fraud Prevention Tools and Solutions:

- PSPs typically provide merchants with access to advanced fraud prevention tools and technologies designed to detect and prevent fraudulent transactions in real time. These may include machine learning algorithms, artificial intelligence (AI) systems, device fingerprinting, and behavioral analytics that analyze transaction patterns and identify suspicious activity.

- PSPs may offer fraud scoring and risk assessment services to evaluate the likelihood of fraud for each transaction and flag high-risk transactions for further review.

Chargeback Monitoring and Alerts:

- PSPs often offer chargeback monitoring and alert services that notify merchants of impending chargebacks or disputes. By providing early detection and prompt alerts, merchants can resolve issues and prevent chargebacks before they occur.

- Some PSPs may also offer chargeback representation services, helping merchants in disputing invalid chargeback claims and providing documentation and evidence to support their case.

Transaction Monitoring and Analysis:

- PSPs may offer transaction monitoring and analysis services to help merchants identify patterns and trends in transaction data that may show fraudulent activity or potential chargeback risks. By analyzing transaction data in real time, merchants can detect anomalies and take corrective action to prevent chargebacks.

- Some PSPs provide merchants with user-friendly reporting and analytics tools that offer insights into chargeback trends, patterns, causes, and areas of improvement.

Enhanced Authentication and Security Measures:

- Enhanced authentication and security tools, such as 3D Secure authentication protocols, verify cardholders’ identities and reduce the risk of unauthorized transactions. These tools offer added layers of authentication, which helps merchants prevent fraudulent transactions and minimize chargeback risks.

- PSPs may offer network tokenization, which replaces sensitive card details with unique digital tokens, reducing the risk of data breaches and unauthorized access to cardholder information.

Dispute Resolution Assistance:

- If there is a chargeback or dispute, PSPs often help merchants navigate the chargeback process and resolve disputes effectively. This may include providing access to chargeback management tools, offering dispute resolution best practices, and helping merchants prepare compelling evidence to support their cases.

- Some PSPs may also offer chargeback mediation services, acting as intermediaries between merchants and card issuers to help resolve disputes and achieve favorable outcomes.

By offering these value-added services and solutions, PSPs empower merchants to proactively manage and prevent chargebacks, protect their businesses against fraud and disputes, and build trust and credibility with their customers and payment partners.

In conclusion, chargebacks present a significant challenge for merchants in the digital age, but by understanding the top scenarios and implementing proactive prevention strategies, businesses can protect themselves and keep trust with their customers. Partnering with a trustworthy and experienced PSP that offers fraud prevention tools and chargeback prevention solutions is crucial. Merchants must apply transparent policies, share comprehensive documentation, and provide excellent customer service to mitigate chargeback risk and prevent financial and reputational risk.

If the information in this blog raised any questions about ways in which you could prevent chargeback risk, do not hesitate to contact one of our experts via [email protected]

******

This article was written by @SandeCopywriter on behalf of Segpay Europe.