Pay by Bank transactions – also known as Bank Transfers, A2A, or Direct Bank Payments – are cardless payment methods that allow customers to pay directly from their bank account to the merchant’s bank account through Open Banking. It is offered by banks and Payment Service Providers (PSPs) in partnership with payment networks or intermediaries, and it is prevalent in Europe. This online payment method is very straightforward and fraud-resistant.

Here is how the Pay by Bank method works:

Source: Finzly.com

Checkout Selection: During the checkout process on a merchant’s website or app, the customer selects a Pay by Bank method and is directed to a list of banks.

Bank Selection: The customer selects their preferred bank from a list that a PSP usually provides.

Authentication: Customers are redirected to their familiar online banking portal or mobile banking app. They log in using their online banking credentials, such as their username and password, or through biometric authentication (fingerprint, iris, etc.).

Payment Authorization: After logging in, the customer authorizes the payment. This may involve confirming the transaction amount and providing additional security information their bank requires, such as a one-time passcode sent via SMS or email.

Payment Processing: Once the customer authorizes the payment, the funds are transferred directly from the customer’s bank account to the merchant’s bank account.

Confirmation: After processing the payment, the customer and the merchant receive transaction confirmation. The merchant starts to process the order or provides immediate access to the purchased goods or services.

Transaction Settlement: The PSP or intermediary ensures that the funds are settled between the customer’s and merchant’s banks, typically through the banking system’s clearing and settlement processes.

Pay Bank transactions are user-friendly and secure for PSPs, merchant, and their customers, who don’t need to fill out private and sensitive information. This method reduces chargeback risk compared to other payment methods.

How do PSPs and merchants benefit from Pay by Bank transactions?

- Expanded Payment Options: By providing Pay by Bank payment methods, PSPs can offer their merchants a broader range of payment options to attract new customers. This leads to better conversion rates and increased customer satisfaction as shoppers have more choices at checkout.

- Reduced Fraud Risk: Since customers authorize payments directly through their bank’s secure online banking portal, there is less fraud risk. This helps PSPs and their merchants minimize losses due to chargebacks and unauthorized transactions. It also saves merchants financial and reputational risk and the costs of managing disputes.

- Lower Processing Fees: Pay by Bank transactions typically involve lower processing fees compared to other payment methods (e.g., card transactions), especially for high-value purchases. Since these transactions bypass credit card networks and associated interchange fees, merchants can save money on transaction costs, especially for high-value purchases.

- Faster Settlement: Pay by Bank transactions often offer real-time or near-real-time settlement. This improves cash flow, as funds from bank transfers can be deposited into the merchant’s account in real-time. This enables merchants to access revenue fast and manage their finances more effectively.

- Enhanced Security: Pay by Bank transactions use the improved security features of online banking platforms, such as multi-factor authentication and encryption, to protect sensitive customer data and transactions. By offering a secure payment method, PSPs can build trust with merchants and customers, leading to long-term relationships and repeat business. For the same reasons, merchants build customer trust and reduce fraud risk and vulnerability to data breaches.

- Compliance with Regulations: Pay by Bank transactions help PSPs and merchants comply with regulatory requirements, such as Strong Customer Authentication (SCA) under the EU’s Payment Services Directive 2 (PSD2). These transactions often use SCA methods, such as biometric verification or one-time passcodes, which comply with SCA requirements. This helps both PSPs and merchants comply with strict EU regulations.

- Competitive Advantage: PSPs gain a competitive advantage from competitors who do not offer merchants this very secure and convenient payment method, which is especially popular in Europe. PSPs strengthen their position in the competitive payment industry by staying ahead of market trends and meeting customer demands for convenient and secure payment methods. Merchants attract customers who prefer to pay directly from their bank accounts because they are concerned about sharing sensitive card information online, because they do not have credit cards, or simply because they prefer the convenience of the Pay by Bank method.

Bank payment methods offer PSPs and Merchants lower costs, reduced risk, faster settlement, enhanced security, competitive advantage, and broader customer reach. This is why including this method in your portfolio is a great business strategy.

Popular Pay by Bank Methods in Europe

Pay by Bank methods have become extremely popular in Europe. Pay by Bank is now one of the top 5 payment methods in the UK, Netherlands, Finland, Spain, and Germany, with one-third of those aged 18-29 using it daily or weekly, according to research published at the end of March this year. In many EU countries, fraud figures have dropped or stabilized. This is reflected in global fraud statistics, where the EU scores much better than other regions where fraud – particularly chargeback fraud – is rampant.

Let’s have a look at some of the most popular Pay by Bank payment methods in Europe:

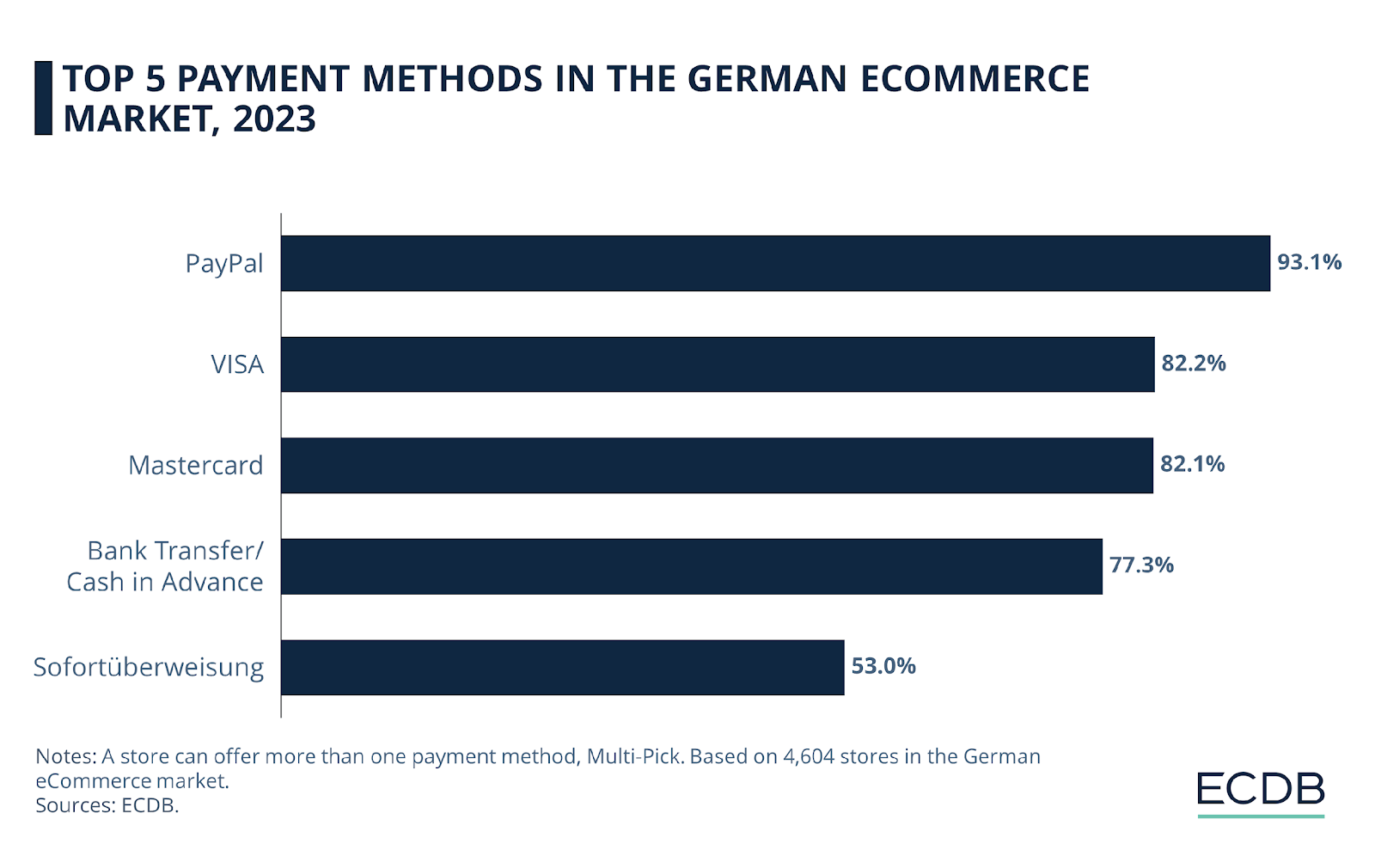

- SOFORT Banking (now Klarna): Sofort GmbH has been acquired by the Klarna Group. Sofort Direct Banking, also known as Pay Now with Klarna, is immensely popular in Germany and has conquered many other European countries. Its 85 million users mainly live in Germany, Austria, Italy, Spain, Belgium, and The Netherlands, but Sofort is also used in many other countries. If we look at the stats below, we learn that Sofort is Germany’s fifth most popular online payment method in Europe’s 2nd largest e-commerce market (after the UK).

- Giropay: Giropay is extremely popular in Germany. Several German banks support it and offer shoppers a convenient and secure Pay by Bank method. Its 45 million users live in Germany, the USA, Switzerland, the Netherlands, and the UK. With a growing % market share of 17%, Giropay is one of the top e-commerce payment methods in Germany, according to eCommerceDB. Merchants receive a payment guarantee straight after successful Giropay transactions (up to €10,000)

- iDEAL: iDEAL is an interbank system local to the Dutch market and allows shoppers to use their bank account for online purchases. iDEAL was launched two decades ago and is covered by all central Dutch consumer banks. It has been the Netherlands’ most popular e-commerce payment method for years. Due to its popularity, card use in the Netherlands needs to be improved compared to the rest of Europe. The same can be said of e-wallet methods like PayPal. The immense popularity of this Pay by Bank method is one of the reasons why the Netherlands has relatively low fraud figures.

- Bancontact: Although PayPal is extremely popular in Belgium, Bancontact, a direct Pay by Bank method, is widely accepted by merchants in Belgium. Belgians love to pay with Bancontact or Payconiq. The use of this method doubled from 1 billion to 2.3 billion transactions over the past ten years.

- Faster Payment Service (FPS) was launched in 2008 to enable instant Bank-to-Bank mobile, internet, phone, and standing order payments to move quickly and securely between UK bank accounts 24/7/365 a year.

- The Pay by Bank app is an easy-to-use British payment method that features real-time authorization. Shoppers make payments directly from their UK bank account. There is no need to sign up for Pay by Bank because it uses existing bank apps installed on mobile phones. Merchants do not need to handle sensitive information; this app fully complies with the EU’s PSD2 Directive.

- EPS (Electronic Payment Standard): EPS is the most popular Pay by Bank method in Austria. It enables customers to pay directly from their bank accounts using their online banking credentials. Most Austrian banks support EPS, which is widely accepted by merchants. With 80% of online shoppers in Austria using EPS, integrating this payment method grants businesses access to a large, loyal customer base.

- Przelewy24 (P24): Przelewy24 is a popular direct banking payment method in Poland. It is widely accepted by merchants and offers a secure and convenient payment experience. This platform is integrated with more than 165 banks in Poland and includes a variety of payment options, including Pay by Bank, credit and debit card transactions, text message payments, and prepaid cards.

- Trustly: Swedish fintech Trustly is a leader in bank transfer payments in Europe, providing online banking in the Baltic and Nordic regions, Spain, and the UK. All central European banks support it. In 2023, Trustly saw a significant surge in its transaction value, achieving a 79% increase to $58 billion, up from $33 billion in the previous year.

- Swish is a popular mobile payment system in Sweden that allows users to make instant, secure transfers directly from their bank accounts. It is used for both online and in-person transactions. Launched in 2012, Swish was developed by collaborating with all central Swedish banks.

Last year, Currence iDEAL and PQI, a Luxembourg-based payment solutions provider that served iDEAL in the Netherlands, Bancontact Payconiq Company in Belgium, and Payconiq in Luxembourg, were acquired by the European Payment Initiative (EPI) to establish a new innovative, and unified payment solution for Europe.

SEPA (Single Euro Payments Area) Direct Debit (SEPA DD)

SEPA DD is a bank account-based payment method for e-commerce and recurring payments across the Eurozone. SEPA DD is a common choice because it simplifies recurring payments, especially across borders within the SEPA area. Subscription businesses can use SEPA DD to attract young shoppers, and compared to card payments, it applies low fees for domestic and cross-border payments. SEPA Direct Debit payments are subject to an eight-week “no questions asked” refund period for customers. Businesses must implement processes to address SEPA’s chargeback rules, which can differ from credit card chargebacks.

What lessons can the USA learn from Europe?

The American online payment market is still dominated by Card Payments, PayPal, and Digital Wallets. However, developments and trends in the European market offer some key lessons.

The popularity of Pay by Bank methods through Open Banking is leading to a more secure, cost-effective, and inclusive payment landscape. Enhanced security and consumer trust driven by strong customer authentication (SCA) significantly mitigate fraud risk, and European regulations, like PSD2 and SCA, improve security. Implementing similar measures in the US could improve consumer confidence in digital payments.

Lower transaction fees are applied to Pay by Bank methods because these methods do not rely on the card networks. This cost-saving benefit is especially crucial for small and medium-sized businesses, enabling them to distribute resources more effectively. Lower transaction costs can also stimulate a broader adoption of digital payments among US merchants. The efficiency of real-time payment processing in Europe provides merchants with immediate access to funds. This improves cash flow for businesses. Faster transaction settlement can streamline operations and enhance liquidity management for US companies.

Consumer convenience is another significant advantage. The Pay by Bank method offers a seamless, user-friendly experience, which can boost customer satisfaction and conversion rates. By simplifying the payment process, US payment systems can improve the overall customer experience, encouraging more frequent use of digital payment options.

Open Banking in Europe also promotes financial inclusion by providing shoppers without credit or debit cards access to banking services. The US can expand financial services to underbanked populations by adopting bank-based payment methods, ensuring broader access to the digital economy. As seen with PSD2 in Europe, a robust regulatory framework can encourage innovation and competition in the US financial sector. Standardizing Open Banking practices can drive the development of secure and efficient Pay by Bank solutions.

Collaboration among European banks has been crucial for the success of Open Banking. US banks can benefit from similar cooperative efforts between banks. In July 2023, the Federal Reserve launched the FedNow Service, an instant payments infrastructure that allows participating banks and credit unions to send and receive transactions within seconds, 24/7. About 470 banks and credit unions joined the FedNow network in early February 2024.

By learning from Europe’s experience with Pay by Bank methods and Open Banking, the US can significantly improve its payment systems and offer more secure, efficient, and inclusive payment solutions.

For more information, do not hesitate to contact our payment experts via:

*********

This article was written by @SandeCopywriter on behalf of Segpay Europe.